Tax-Exempt Strategies: Q3 2024

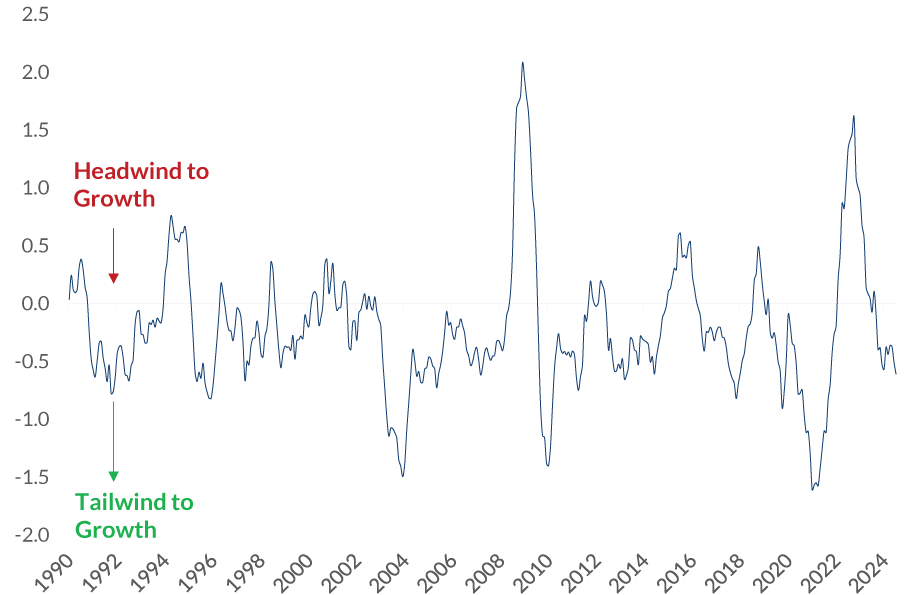

As we head into the final stretch of 2024, the global economic outlook remains largely positive, with the U.S. economy showing resilience amid some moderation. Market indicators from the City National Rochdale (CNR) Speedometers® highlight steady economic and financial trends, including recent upgrades to our monetary policy and consumer sentiment dials. Projections for U.S. GDP growth range between 1.75% and 2.25% in 2024. Corporate profits are anticipated to rise 9%-12%, with inflation moderating to around 2.5%-3%, even as Federal Reserve rate cuts start to take effect. While some concerns linger, the broader market appears to be well-supported.

With election year uncertainty in focus, market patterns tend to shift as volatility rises before Election Day. Historically, stock prices may experience a dip of around 3% between August and November, but this is often followed by a strong rebound once election results are clear. Markets typically rise over November and December as uncertainty lifts. Although political events can introduce some noise, they are generally less impactful on market direction than core fundamentals like corporate profits, interest rates and monetary policy. There is also no notable correlation between party control and returns. The stock market is not partisan.

Source: Federal Board of Reserve, as of September 2024.

Information is subject to change and is not a guarantee of future results.

In terms of sectors, technology has been a star performer, driving much of the market’s gains, but there have been questions around valuation and narrow leadership. Still, AI is likely to continue its robust adoption and growth. The first half of 2023 saw AI-related investments reach $120 billion, with forecasts suggesting that figure could grow to $160 billion by 2025. AI’s transformative potential is significant, with an expected contribution of $2.6 trillion to $4.4 trillion annually across industries such as marketing, healthcare and software development.

Globally, markets have experienced a mixed year, with pockets of outperformance in Europe and emerging markets. However, the U.S. has consistently outperformed, rising more than 5% over international markets since July1. While international markets have shown promise at times, opportunities have often been fleeting, as regional conflicts, higher inflation and lower growth prospects have dampened performance.

Despite the difficulty in the international investment landscape, the world economy remains on track. The services sector has been the engine of global growth, while manufacturing has struggled to keep pace, even experiencing contraction in some areas. However, the outlook is positive that any slowdown in growth will be countered by over half of the world’s central banks embracing easing cycles. And, while the Chinese economic outlook remains highly uncertain, China’s recent stimulus measures are expected to bolster global growth in the upcoming year, providing another source of upside potential.

Turning back to the U.S., financial conditions have improved notably, easing some of the tightening from earlier in the year. The Federal Reserve’s shift toward an easing cycle has benefited the credit markets, which remain healthy. Corporate earnings are solid, and bond issuance has increased compared to last year. This more supportive backdrop from the Fed could act as a tailwind for continued market stability, lowering the risk of significant market disruptions. Should this easing trend persist, the Fed may well achieve its goal of a soft landing without the need for drastic economic adjustments.

The economic landscape is further supported by a resilient U.S. labor market. September saw nonfarm payroll growth that exceeded expectations, and revisions to previous months’ data indicate a stronger job creation trend than initially thought. The unemployment rate has declined to 4.1%2, and household employment is on the rise. While some concerns about labor market momentum remain, anticipated rate cuts should help support further job growth and bolster consumer confidence as we approach year-end.

Real consumer spending has also remained robust, ticking up in recent months and projected to grow by 2.4% in 2024 and 1.9% in 20253. The underlying strength in consumer demand, particularly in retail, suggests a positive trend for continued economic growth. Consumer credit conditions remain stable, despite increases in delinquencies in lower income quartiles, household debt service levels are near historical lows, and wealth has increased across all income groups. Although credit card balances recently topped $1 trillion, when adjusted for inflation, this rise has been minimal over the past 25 years. Even in the housing sector, where limited inventory has driven up prices, conditions appear poised to improve as rates ease.

Financial markets are another beneficiary of Federal Reserve rate cuts. In fixed income, short-term Treasury yields are beginning to decline, and the yield curve is gradually normalizing. Credit spreads in corporate bonds remain stable, reflecting strong demand from investors and solid credit fundamentals. On the equity side, Fed rate cut expectations have supported a rotation in market leadership, which has broadened YTD returns away from tech stocks.

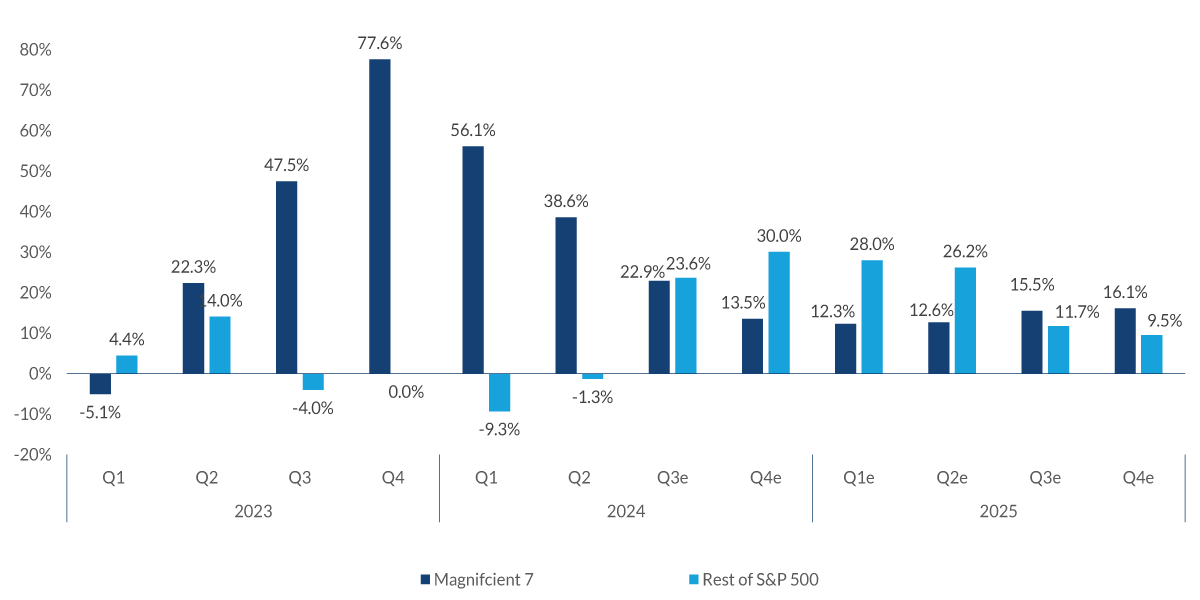

Equity market performance has also been bolstered by strong earnings growth across multiple sectors. Q2 earnings demonstrated broad-based improvement, with 9 out of 11 sectors showing year-over-year gains (see chart 2). Initially, technology stocks led the rally in 2023, but more recently, earnings estimates have begun to accelerate across a broader market spectrum.

Source: FactSet, as of September 2024. Information is subject to change and is not a guarantee of future results.

Past performance is not a guarantee of future results.

The broadening of market leadership is a promising signal for future equity gains, indicating that other sectors are beginning to contribute meaningfully to overall performance. In the U.S., sectors like utilities and real estate have performed well in the third quarter, demonstrating gains while more traditional growth sectors have taken a breather. Utilities, in particular, have seen an unusual surge, outperforming during an up market — a pattern typically associated with market declines. Meanwhile, value sectors are showing signs of strength, indicating a potential rotation as we close out the year.

Looking forward, the combination of easing financial conditions, strong corporate earnings and ongoing economic growth paints an optimistic backdrop for market returns as we head into the final months of 2024. While election uncertainties may introduce some short-term volatility, history suggests a quick recovery. With strong AI investment trends, a stable credit landscape and solid labor market conditions, the outlook is set for a strong conclusion to the year and a promising start to 2025.

1Data as of the S&P 500; MSCI EAFE, as of October, 2024

2Data as of The Bureau of Labor Statistics (BLS), as of September, 2024.

3Data as of the Bloomberg consensus estimates, as of October, 2024.

Important Information

The views expressed represent the opinions of City National Rochdale, LLC (CNR) which are subject to change and are not intended as a forecast or guarantee of future results. Stated information is provided for informational purposes only, and should not be perceived as personalized investment, financial, legal or tax advice or a recommendation for any security. It is derived from proprietary and non-proprietary sources which have not been independently verified for accuracy or completeness. While CNR believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations,estimates, projections, and other forward-looking statements are based on available information and management’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions which may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements.

All investing is subject to risk, including the possible loss of the money you invest. As with any investment strategy, there is no guarantee that investment objectives will be met, and investors may lose money. Diversification may not protect against market risk or loss. Past performance is no guarantee of future performance.

There are inherent risks with equity investing. These risks include, but are not limited to stock market, manager, or investment style. Stock markets tend to move in cycles, with periods of rising prices and periods of falling prices.

There are inherent risks with fixed income investing. These risks may include interest rate, call, credit, market, inflation, government policy, liquidity, or junkbond. When interest rates rise, bond prices fall.

Bloomberg risk is the weighted average risk of total volatilities for all portfolio holdings. Total Volatility per holding in Bloomberg is ex-ante (predicted) volatility that is based on the Bloomberg factor model.

Municipal securities. The yields and market values of municipal securities may be more affected by changes in tax rates and policies than similar income-bearing taxable securities. Certain investors’ incomes may be subject to the Federal Alternative Minimum Tax (AMT), and taxable gains are also possible. Investments in the municipal securities of a particular state or territory may be subject to the risk that changes in the economic conditions of that state or territory will negatively impact performance. These events may include severe financial difficulties and continued budget deficits, economic or political policy changes, tax base erosion, state constitutional limits on tax increases and changes in the credit ratings.

City National Rochdale, LLC is an SEC-registered investment adviser and wholly-owned subsidiary of City National Bank. Registration as an investment adviser does not imply any level of skill or expertise. City National Bank is a subsidiary of the Royal Bank of Canada.

© 2024 City National Bank. All rights reserved.

Index Definitions

S&P 500 Index: The S&P 500 Index, or Standard & Poor’s 500 Index, is a market-capitalization-weighted index of 500 leading publicly traded companies in the US It is not an exact list of the top 500 US companies by market cap because there are other criteria that the index includes.

The MSCI EAFE Index is a stock market index that measures the equity market performance of developed markets outside of the U.S. & Canada.

DJ US Select Dividend Index: The Dow Jones U.S. Select Dividend Index aims to represent the U.S.’s leading stocks by dividend yield.

Bloomberg Municipal Bond Index: The Bloomberg US Municipal Bond Inde x measures the performance of in vestment grade, US dollar-denominated, long-term tax-exempt bonds.

Bloomberg Municipal High Yield Bond Inde x: The Bloomberg Municipal High Yield Bond Inde x measures the performance of noninvestment grade, US dollar-denominated, and non-r ated, tax-exempt bonds.

Bloomberg Investment Grade Index: The Bloomberg US In vestment Grade Corporate Bond Index measures the performance ofinvestment grade, corporate, fixed-rate bonds with maturities of one y ear or more.

G0BA Index: ICE BofA US Treasury Bill Index:The index measures the performance of US dollar denominated US Treasury Bills publicly issued in the US domestic market. Qualifying securities must have at least one month remaining term to final maturity and a mini mum amount outstanding of $1 billion. It is capitalization-weighted.

G0Q0 Index: ICE BofA US Treasury Index: ICE BofA US Treasury Bill Index:The index measures the performance of US dollar denominated US Treasury Bills publicly issued in the US domestic market. Qualifying securities must have at least one month remaining term to final maturity and a minimum amount outstanding of $1 bi llion. It is capitalization-weighted.

LUACTRUU Index: Bloomberg US Corporate Total Return Value Unhedged USD: The Bloomberg US Corporate Bond Index measures the investment grade, fixed-rate, taxable corporate bond market. It includes USD denominated securities publicly issued by US and non-US industrial, utility and financial issuers.

LF98TRUU Index: Bloomberg US Corporate High Yield Total Return Index Value Unhedged USD. Bloomberg: LF98TRUU Index: The Bloomberg US Corporate High Yield Bond Index measures the USD-denominated, high yield, fi xed-rate corporate bond market.

Securities are classifi ed as high yield if the middle rati ng of Moody’s, Fitch and S&P is Ba1/BB+/BB+or below. Bonds from issuers with an emerging markets country of risk, based onBloomberg EM country defi niti on, are excluded. This is the total return index level.

Indexes are unmanaged and do not reflect a deduction for fees or e xpenses. Investors cannot invest directly in an index.

Definitions

Yield to Worst (YTW) is the lower of the yield to maturity or the yield to call. It is essentially the lowest potential rate of return for a bond, excluding delinquency or default.

P/E Ratio: The price-to-earnings ratio (P/E ratio) is the ratio for valuing a company that measures its current share price relative to its earnings per share (EPS).

The 4P analysis is a proprietary framework for global equity allocation. Country rankings are derived from a subjective metrics system that combines the economic data for such countries with other factors including fiscal policies, demographics, innovative growth and corporate growth. These rankings are subjective and may be derived from data that contain inherent limitations. MSCI Emerging Markets Asia Index is a free float-adjusted market capitalization index that is designed to measure equity market performance in the Asian emerging markets.

The Magnificent Seven stocks are a group of high-performing and influential companies in the U.S. stock market: Alphabet, Amazon, Apple, Meta Platforms, Microsoft, NVIDIA, and Tesla.

City National Rochdale Proprietary Quality Ranking formula: 40% Dupont Quality (return on equity adjusted by debt levels), 15% Earnings Stability (volatility of earnings), 15% Revenue Stability (volatility of revenue), 15% Cash Earnings Quality (cash flow vs. net income of company) 15% Balance Sheet Quality (fundamental strength of balance sheet).

*Source: City National Rochdale proprietary ranking system utilizing MSCI and FactSet data. **Rank is a percentile ranking approach whereby 100 is the highest possible score and 1 is the lowest. The City National Rochdale Core compares the weighted average holdings of the strategy to the companies in the S&P 500 on a sector basis. As of September 30, 2022. City National Rochdale proprietary ranking system utilizing MSCI and FactSet data.

BPS: A basis point (BPS) is used to indicate changes in the interest rates of a financial instrument. Basis points are typically expressed with the abbreviations “bp,” “bps,” or “bips.”

A consensus estimate is a forecast of a public company’s projected earnings based on the combined estimates of all equity analysts that cover the stock.

Bureau of Labor Statistics(BLS): The BLS is a federal agency that collects and disseminates important information about labor, wages, prices, and productivity.

© 2024 City National Bank. All rights reserved.

Non-deposit investment Products are: • not FDIC insured • not Bank guaranteed • may lose value

If you have a client with more than $1 million in investable assets and want to find out about the benefits of our intelligently personalized portfolio management, speak with an investment consultant near you today.

If you’re a high-net-worth client who's interested in adding an experienced investment manager to your financial team, learn more about working with us here.